Bullish Momentum Holds Firm in Global Asset Allocation

Echoing previous updates (see here and here, for example), an ETF-based proxy for monitoring the directional bias of multi‑asset‑class strategies continues to skew positive, based on the ratio of two funds: an aggressive asset allocation strategy (AOA) vs… But if this fade for growth relative…

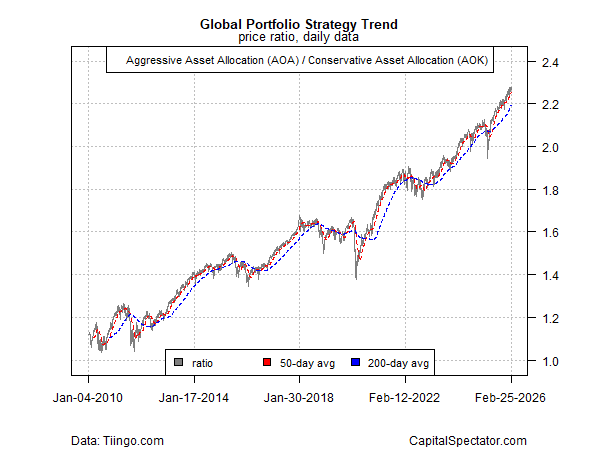

Optimism may seem scarce in the headlines, but a bullish trend still powers global asset‑allocation strategies, based on a set of ETFs through yesterday’s close (Feb. 25).

Although the risk appetite from a global perspective has periodically wavered in recent history, betting against the trend has been a losing proposition. Echoing previous updates (see here and here, for example), an ETF-based proxy for monitoring the directional bias of multi‑asset‑class strategies continues to skew positive, based on the ratio of two funds: an aggressive asset allocation strategy (AOA) vs. its conservative counterpart (AOK).

Looking below the surface, however, reveals substantial changes in leadership as bullish momentum accelerates in foreign stocks relative to US shares. The previous relative strength in American equities (VTI) has fully reversed against stocks in developed markets ex‑US (VEA).

A similarly sharp U‑turn is in progress for US equities (VTI) vs. stocks in emerging markets (VWO).

Another notable change: Within the US stock market, sentiment has recently shifted in favor of large‑cap value (IWD) over large‑cap growth (IWF). Although this turn is significant in that it breaks the long‑running dominance of large‑cap growth, it’s not yet clear if this is yet another short‑term change or the start of a secular trend.

As the chart above shows, there have been several periods since 2010 of short-lived relative strength for large‑cap value that quickly faded. The current pivot into value looks solid so far, but it’s still an open question if this trend signals a durable change in market sentiment.

If the value leadership persists, some analysts say it could have implications for the broader stock‑market outlook.

Stifel’s chief equity strategist, Barry Bannister, warns in a research note this week that some investors view the recent value rebound and growth‑stock weakness “as a sign of cyclical economic recovery, and it may be. But if this fade for growth relative to value accelerates and deepens, the history of ‘secular’ value‑led markets is one of a sharply declining price‑to‑earnings ratio over time, weaker S&P 500 returns and ever greater shocks, often lasting for many years.”

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return![]()

By James Picerno

Author: James Picerno