Early Impact of Iran War Is Low, But Economic Risks Are Rising

The main risks: slower economic growth and higher inflation, driven largely by higher energy prices… US and Israeli officials have said the war could continue for several weeks, which would give the inflationary and slower-growth effects more oxygen… Add in the inflation-related uncertaint…

The economic fallout from the war in Iran has been limited for the US so far. But as the conflict continues, the effects will become increasingly clear.

The main risks: slower economic growth and higher inflation, driven largely by higher energy prices. It’s too early to confidently estimate how the war will influence those factors, but as the war – one week old tomorrow – persists, the macro price tag will surely rise.

Because economic data is reported with a lag, the blowback will take time to show up in official releases. For next month’s first-quarter GDP release, for instance, even if the war continues through the end of March, the effects may be hard to spot.

The Atlanta Fed’s Mar. 2 nowcast of Q1 GDP: +3.0%, marking a solid rebound from the sluggish 1.4% increase in Q4. Revisions are likely before the official April 30 release, but the war-related impact may be modest, given that the attack began late in the quarter.

February data published earlier in the week underscores ongoing strength in private‑sector hiring and services activity. ADP on Wednesday said that companies added 63,000 jobs last month, the strongest monthly gain since July. Meanwhile, the ISM Services Index rose to its highest growth reading in February in nearly four years.

The outlook for Q2 is more vulnerable. US and Israeli officials have said the war could continue for several weeks, which would give the inflationary and slower-growth effects more oxygen. The degree and extent of pain these effects could bring is unclear for now, but markets are already reflecting greater caution relative to the pre-war outlook.

One of the clearest signs of shifting sentiment relates to monetary policy. The rate cuts that were priced in via Fed funds futures for June are now seen as unlikely. September is currently the earliest month in which odds favor an initial cut.

Earlier this week, Cleveland Fed President Beth Hammack called for an extended pause on rate cuts. Part of the calculus is that economic activity appears to be firming in Q1. Add in the inflation-related uncertainty from the war and she sees a stronger case for holding rates steady. “I want to see evidence that we are making progress on the inflation side of our mandate to have more confidence in my forecast,” she said.

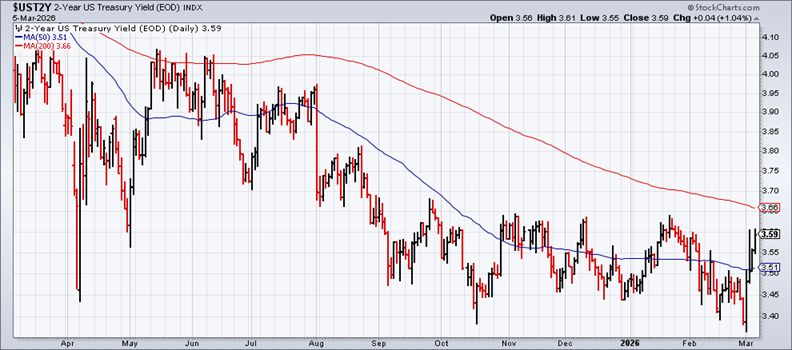

Treasury yields have remained relatively steady since the war started, trading within the range that’s prevailed in recent months. But the market is starting to pick up on the potential for higher inflation. The policy-sensitive 2-year yield has increased every day this week, rising to 3.59% on Thursday.

Higher yields are likely until there are signs that the war, if not ending, is winding down. For now, the opposite seems to be the likely path ahead for the immediate future.

The FT this morning is reporting: Qatar, the world’s second-largest producer of liquified natural gas, says the war will force Persian Gulf energy exports to end “within days.”

“This will bring down the economies of the world,” predicts Saad al-Kaabi, Qatar’s energy minister. “If this war continues for a few weeks, GDP growth around the world will be impacted. Everybody’s energy price is going to go higher. There will be shortages of some products and there will be a chain reaction of factories that cannot supply.”

Hyperbole? Maybe, but making that case that the fallout will be limited is becoming tougher every day the war continues and energy infrastructure in the Gulf comes under additional strain.

Is Recession Risk Rising? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

Author: James Picerno