Bond Market Starting To Push Back On Powell’s Inflation View

Federal Reserve Chairman Jerome Powell may be downplaying inflation risks, but the bond market is signaling skepticism about how quickly price pressures will recede… Although both rates are still trading at middling levels relative to their ranges in recent years, the rapid jump is hard to miss an…

Federal Reserve Chairman Jerome Powell may be downplaying inflation risks, but the bond market is signaling skepticism about how quickly price pressures will recede.

“Inflation expectations do appear to be well anchored beyond the short term, but nonetheless, it’s something we will eventually maybe face the question of what to do here,” Powell said on Monday at a talk at Harvard University. “We’re not really facing it yet, because we don’t know what the economic effects will be, but we’ll certainly be mindful of that broader context when we make that decision.”

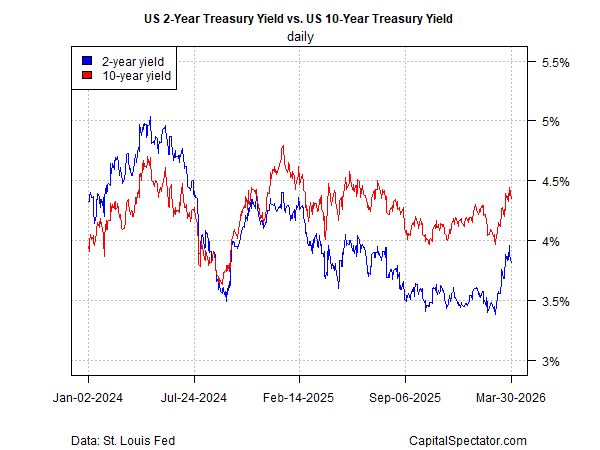

The bond market is already mindful that the risk calculus has changed since the war started. The 2- and 10-year Treasury yields, for example, have shot up since the war started on Feb. 28. Although both rates are still trading at middling levels relative to their ranges in recent years, the rapid jump is hard to miss and is likely driven by concerns that inflation risk at the headline level is rising.

In line with the shifting sentiment, short-term inflation-indexed Treasuries (STIP) are the top performer this year for a set of bond-market ETFs through yesterday’s close (Mar. 30).

Headline inflation will almost certainly pulse higher in the near term in the wake of the sharp runup in energy prices, but some economists predict that the rise will be short-lived.

“Risks to inflation should rise initially but then fall if the shock is large enough, due to demand destruction,” economists at Bank of America Research estimated last week. “Negative wealth effects from a sustained equity selloff would exacerbate downside risks to labor and limit the upside to inflation.”

Rate hikes are still considered unlikely for the near-term outlook, but so are rate cuts, based on the implied probabilities via Fed funds futures.

The Treasury market’s implied inflation forecast via 5-year maturities has been breaking higher relative to the 10-year maturities. The implication: the market expects any increase in inflation pressure to be relatively short-lived. Note, too, that the Treasuries’ inflation outlook has yet to decisively break above recent peaks, which suggests that the crowd is not yet fully convinced that inflation is a threat that will outlast the war’s end.

Meanwhile, the longer the conflict lasts, the less patience the bond market will exhibit for tolerating the Fed’s preference to leave monetary policy as is. In that sense, President Trump has acquired a degree of power to effectively run Fed policy by determining when the war ends. Whether this influence will satisfy his preference for rate cuts, however, remains in doubt for the foreseeable future.

Author: James Picerno