Will Markets Start To Price In Lower Inflation Risk?

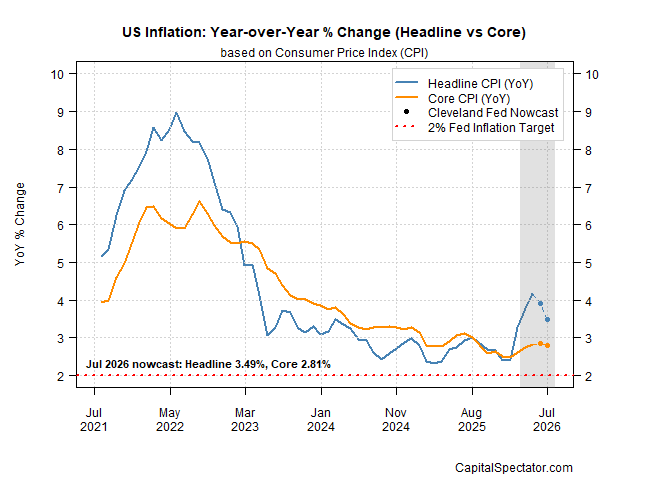

benchmark, marking a return to the level on the eve of the war’s start on Feb…The unwinding of the war premium in oil points to softer inflation expectations, particularly at the headline level, which uses energy costs as inputs… The current inflation nowcasts from the Cleveland Fed anticip…

The Iran war appears to be over, or so the ongoing ceasefire suggests. The oil market is certainly leaning into that view: the price of crude has dropped sharply in recent weeks and begins trading this week at around $70 a barrel for the U.S. benchmark, marking a return to the level on the eve of the war’s start on Feb. 28.

The unwinding of the war premium in oil points to softer inflation expectations, particularly at the headline level, which uses energy costs as inputs. The current inflation nowcasts from the Cleveland Fed anticipate that the year-over-year change in the Consumer Price Index peaked at 4.2% in May and will drop to 3.9% in the upcoming June report and 3.5% in July. Core CPI, which is running at a softer pace, is also expected to ease.

A new round of disinflation will give the Federal Reserve more time to consider the case for a hawkish pivot. Doves argue that rate hikes should be off the table in the wake of oil’s latest slide.

The Fed’s current policy stance has recently shifted to neutral from a modest hawkish tilt, according to The Capital Spectator’s estimate, based on a simple model that uses unemployment and headline CPI—proxies for the central bank’s dual mandate.

Assuming that the recent inflation surge is reversing suggests that the Fed can continue to be patient in deciding how, or if, to adjust monetary policy. A key question for the week ahead: Will the Treasury market validate the view that inflation risk is fading and that rate hikes are no longer needed?

The 2-year Treasury yield is the frontline for monitoring investor sentiment on the policy outlook. As the week begins, this corner of the bond market is pricing in high odds for one or more rate hikes. The 2-year yield ended last week’s trading at 4.18%—close to a one-year high and substantially above the Fed’s 3.50%–3.75% target range.

The Fed funds futures market is pricing in moderately high odds (76%) for no change at the next FOMC meeting on July 29. The outlook turns modestly hawkish for the September rate decision.

Will this week’s market activity lean into the dovish view? Several factors will inform the outcome, starting with the news flow from the Middle East, and so no news will continue to be good news on this front.

The other key variable is the incoming numbers for the U.S. economy, which has been relatively resilient during the war. Will the return of peace (and lower energy costs) further strengthen the economic trend? If so, will that undercut the view that the Fed can leave policy unchanged?

A useful real-time monitor of economic activity is the Dallas Fed’s Weekly Economic Index (WEI), which is currently nowcasting year-over-year GDP growth at around 2.6%. That’s roughly in line with the year-over-year rise previously reported for Q1 growth.

The main takeaway: the case for leaving Fed policy unchanged still looks like a reasonable estimate for the near term, which implies a moderately lower 2-year Treasury yield. The key assumptions supporting this outlook: the ceasefire in the Gulf holds (and broadens into a more durable peace deal), oil exports continue to rebound and normalize, and U.S. economic activity doesn’t accelerate on the back of lower energy costs.

Is Recession Risk Rising? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

Author: James Picerno