June’s Drop in the Yield Premium Faces a Gulf‑Driven Reality Check

In short, the geopolitical shock has reintroduced a level of uncertainty that markets had begun to discount, leaving investors to reassess whether June’s disinflationary signals were a pause rather than a pivot… 10‑year Treasury yield dipped in June after rising for three months, based on…

The market premium for the U.S. 10‑year Treasury yield dipped in June after rising for three months, based on a fair‑value estimate calculated by The Capital Spectator. The decline coincided with last month’s expectations that the war‑driven rise in inflation expectations had peaked. But the resumption of hostilities in the Gulf in recent days has raised questions about whether recent optimism on the inflation outlook is premature.

Military strikes by the U.S. and Iran in the Gulf region have intensified in recent days. The U.S. hit Iran early Wednesday, launching heavier airstrikes and reimposing a naval blockade after Tehran attacked ships in the Strait of Hormuz, a key chokepoint for oil exports. As the two sides traded overnight strikes for a fourth straight night—amid President Trump’s threat of a ground invasion and infrastructure attacks—fears of a full‑scale war escalated on Wednesday.

The threat of renewed fighting may keep oil prices rising, which could slow or reverse the easing inflation trend reported for June, based on the Consumer Price Index (CPI). After running hotter for months, the 1‑year change in headline and core CPI cooled last month for the first time since January. But the revival of a disinflationary impulse may fade or even reverse if the Middle East crisis intensifies.

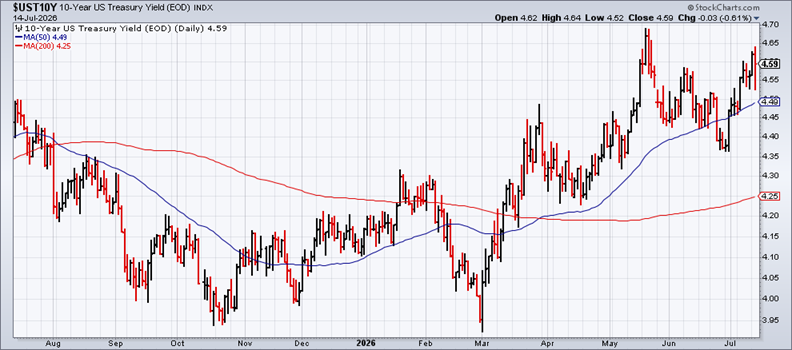

The 10‑year yield continues to trend higher, albeit in fits and starts. In yesterday’s trading, the benchmark rate closed slightly lower, at 4.59%, close to its recent peak near 4.70%.

The market premium for the 10‑year yield slipped to 38 basis points in June, marking the first month‑to‑month decline since February, according to The Capital Spectator’s average estimate for three models. Note that the softer spread was due to a drop in the monthly 10-year yield, in contrast to the model’s fair-value estimate, which continued to rise.

The current premium remains modest by historical standards and implies that the 10‑year note is offering a relatively attractive yield.

One caveat to consider: the model doesn’t factor in geopolitical risk. The renewed hostilities in the Gulf underscore why the recent easing in the market premium may prove fleeting. With the U.S.–Iran conflict again disrupting energy markets and reviving fears of a broader regional war, the inflation outlook is suddenly more fragile than it appeared just weeks ago. Oil remains the key transmission channel, and any sustained rise in crude prices threatens to re‑accelerate inflation expectations, push Treasury yields higher, and widen the market premium anew.

In short, the geopolitical shock has reintroduced a level of uncertainty that markets had begun to discount, leaving investors to reassess whether June’s disinflationary signals were a pause rather than a pivot.

Author: James Picerno