As Inflation Heats Up, the Bond Market Loses Its Cool

The bond market will be the center of attention for investors this week as they assess how much inflation risk is lurking… Official reports already highlight accelerating pricing pressures, driven by Middle East turmoil that has lifted energy costs and raised headline measures of inflation… The …

The bond market will be the center of attention for investors this week as they assess how much inflation risk is lurking. Official reports already highlight accelerating pricing pressures, driven by Middle East turmoil that has lifted energy costs and raised headline measures of inflation. The debate is whether the run‑up in inflation is temporary or reflects a shift that will persist. Bound up with that question is how the Federal Reserve should respond.

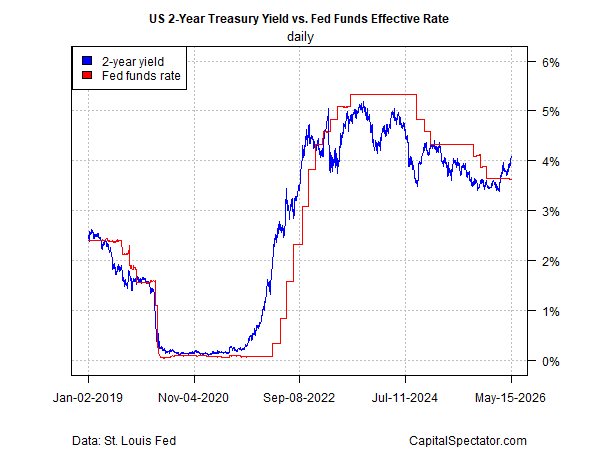

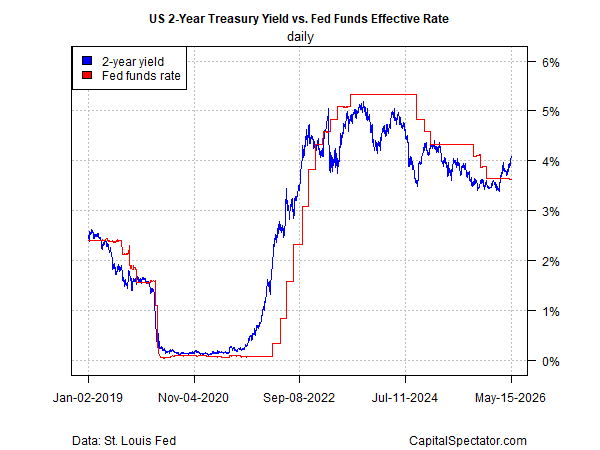

The Treasury market has already decided that tighter monetary policy is necessary. The policy‑sensitive 2‑year yield soared last week, rising above 4.0% for the first time in nearly a year. The jump is a sign that the bond market expects a hawkish pivot from the Fed.

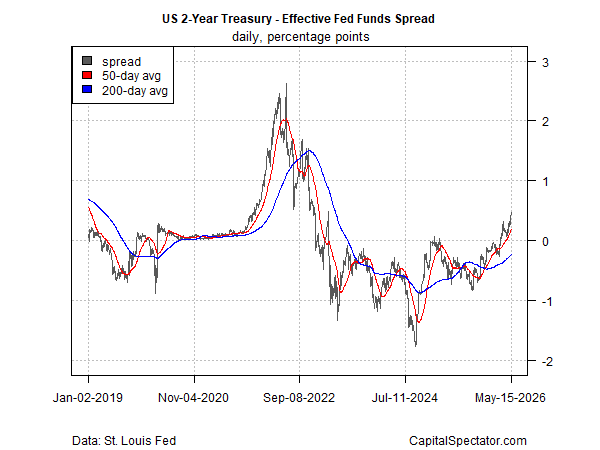

For a clearer view of how market conditions have changed, the chart below shows the spread between the 2‑year yield and the effective Fed funds rate (the volume‑weighted median of overnight Federal funds transactions). This gap has increased to a three‑year high—nearly half a percentage point.

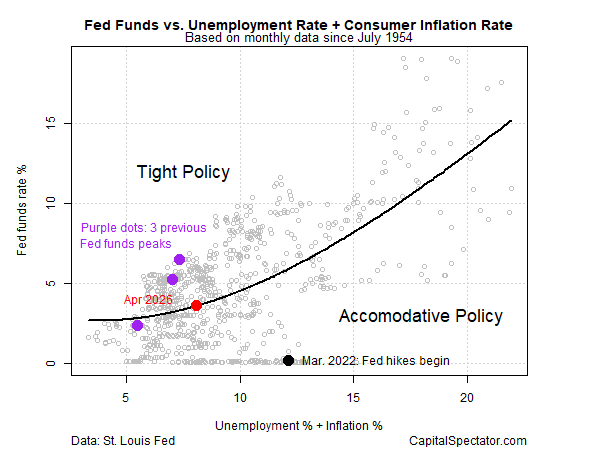

The Capital Spectator’s rough estimate of current Fed policy suggests a neutral stance, based on a simple model that compares the target rate to unemployment and inflation—the two components of the central bank’s dual mandate. A month ago, the estimate indicated that policy was slightly tight. The key takeaway: ongoing inflation risk appears set to shift policy into a dovish stance, assuming the Fed continues to leave rates unchanged.

Fed funds futures are still pricing in high odds of no change for the next several policy meetings. The highest confidence for standing pat applies to the upcoming June 17 FOMC meeting—futures are estimating a 99% probability of keeping rates steady. A 90‑plus percent probability of no change is currently assigned to the July meeting.

The tension between the 2‑year yield and expectations for Fed funds will be closely monitored in the days and weeks ahead. A capitulation on one side or the other would be notable, although analysts seem to be leaning toward the view that expectations for a Fed rate hike are building.

“I do think there is a real fear that inflation is kind of embedded in the economy going forward,” said Peter Tuz, president of Chase Investment Counsel in Charlottesville, Virginia.

“A new inflation regime awaits [Kevin] Warsh,” the new Fed chief, writes Joseph Brusuelas, chief economist at RSM US.

“The fact that we are now seeing data backing up inflationary fears that have been in the market since the Middle East conflict started is key,” said Nick Twidale, chief markets analyst at ATFX Global.

A repricing of Fed funds futures to reflect the shift in sentiment may prove to be the decisive factor prompting a capitulation by the doves.

Author: James Picerno