Cooler June Inflation Clashes with Fresh Middle East Risk

Federal Reserve officials are talking tough on inflation, but the outlook for monetary policy is still cloudy amid murky geopolitical and economic conditions… Governor Christopher Waller set the tone on Monday, noting that raising interest rates may be necessary in the “near term” if inflation…

Federal Reserve officials are talking tough on inflation, but the outlook for monetary policy is still cloudy amid murky geopolitical and economic conditions.

The possibility of a hawkish pivot came into focus this week after comments from three of the central bank’s policymakers. Governor Christopher Waller set the tone on Monday, noting that raising interest rates may be necessary in the “near term” if inflation continues running well above the 2% target. “Sternly staring at inflation until it melts before our withering gaze is not an option,” he told the New York Association for Business Economics.

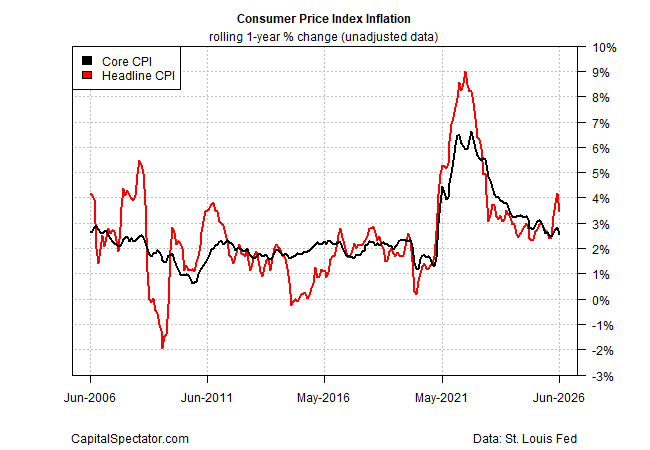

On Wednesday, the government published data that highlighted cooler inflation figures for June, which ease the pressure for rate hikes, at least on the margin for the immediate future. The year-on-year change in the headline measure of the consumer price index (CPI) moderated for the first time since January. Core CPI, which strips out food and energy and is said to be a more robust measure of the pricing trend, also fell back.

Shortly after the CPI report was released yesterday, Fed Chair Warsh told the House Financial Services Committee that he and his colleagues “have no tolerance for persistently elevated inflation.”

Later on Wednesday, Fed Governor Lisa Cook said, “I see it as prudent to give a bit more time to observe how inflation unfolds from here.” Speaking at the Exchequer Club of Washington, D.C., she added: “Going forward, though, I believe the risks continue to be strongly weighted toward higher inflation for at least two reasons.”

One reason is related to the rapid rise in the AI-driven building of data centers, she noted. The second is “the recent big supply shocks—tariffs and the Middle East conflict—that risk leading to persistently higher inflation.”

Despite the hawkish comments this week, yesterday’s CPI data strengthened the market’s view that the Fed would leave its target rate unchanged at the next FOMC meeting on July 29. The Fed funds futures market is currently estimating a 90% probability of standing pat later this month. The outlook for a rate change at the September meeting, by contrast, is roughly a coin toss estimate.

The return of military strikes by the U.S. and Iran in the Gulf region in recent days raises uncertainty about the disinflationary pulse that emerged in the June CPI report. Absent the war, core inflation’s trend would likely ease in the months ahead, based on a model updated each month in The US Inflation Trend Chartbook, which is part of the research service for subscribers to The U.S. Business Cycle Risk Report, an affiliate publication of The Capital Spectator. In line with recent updates, the model’s current estimate shows the one-year change for core CPI easing in the near term, based on the point forecasts. Keep in mind, however, that the model is purely econometric and doesn’t factor in geopolitical risk.

The question is whether the softer inflation in June is outdated now that military actions in the Middle East have resumed, curtailing energy exports through the Strait of Hormuz again and driving up oil prices. Because of the renewed fighting, tanker traffic through Hormuz fell late last week, abruptly halting a brief recovery that followed the fragile ceasefire between the U.S. and Iran — an agreement that has collapsed this week.

The U.S. benchmark for crude oil (WTI) has rebounded in recent days to just under $80 a barrel, but remains far below the levels reached earlier in the war. For the moment, the inflation impulse from energy remains relatively moderate.

The clock is ticking, warns Fatih Birol, executive director of the International Energy Agency (IEA). He predicts the global economy faces economic impacts within weeks as Middle East tensions re-escalate and tanker traffic through the Strait of Hormuz halts.

“If the Strait of Hormuz remains closed, we may again have some difficulty for global economies, including those in the region, developing nations, and Asia,” Birol explained in an interview with Bloomberg yesterday. “It is not months, it is weeks,” before major economic challenges return, he advised.

A new round of an energy shock could slow economic activity, and in turn translate into a disinflatinonary pulse, eventually. In the near term, however, pricing pressure would probably rebound if the Middle East crisis continues to deepen.

Is Recession Risk Rising? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

Author: James Picerno