Energy Stocks Are Soaring, Too

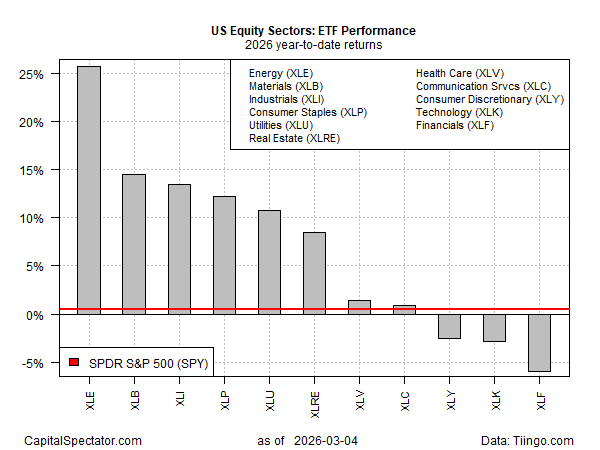

Driven by rising oil and gas prices, energy shares are the leading sector performer by far, based on a set of ETFs through yesterday’s close (Mar…Materials (XLB) and industrials (XLI) are distant second‑ and third‑place sector performers this year, followed by consumer stap…

The war in Iran has upended expectations about winners and losers in the US stock market, redirecting equity investment flows into energy, materials, and industrials. How long this leadership rotation lasts will likely be determined by the course and duration of the war. Meantime, old‑economy stocks are back in vogue.

Driven by rising oil and gas prices, energy shares are the leading sector performer by far, based on a set of ETFs through yesterday’s close (Mar. 4). The State Street Energy Select Sector SPDR ETF (XLE), a Big Oil proxy, has surged more than 25% year to date. That compares with a near‑flat performance for the broad stock market via the SPDR S&P 500 ETF (SPY), which is holding on to a fractional 0.5% gain so far in 2026.

Materials (XLB) and industrials (XLI) are distant second‑ and third‑place sector performers this year, followed by consumer staples (XLP), utilities (XLU), and real estate (XLRE). The remaining sectors are close to flat or underwater. The biggest loser: financials (XLF), down 6.0% year to date.

The attitude shift could be short‑lived, depending on how the war unfolds from here. Many analysts assume the conflict will end soon, in which case the current sector leaders could lose their performance crowns and a return to AI and digital‑economy themes would ensue.

Perhaps—but it’s already clear that the US and Israeli strike on Iran is no quick surgical attack. The conflict is now five days in and the odds appear low for a resolution in the immediate future.

Both the US and Israel have publicly said that a weeks‑long war is possible, perhaps even likely. Top Pentagon officials on Wednesday warned that the war could become a longer conflict and that the fighting is “far from over.” Defense Secretary Pete Hegseth said the conflict could last as long as eight weeks.

“We’re preparing for several long weeks,” acknowledged a senior Israeli military officer.

The duration of the war is the key variable for risk appetite and how markets evolve from here.

“If disruption is relatively short‑lived, history suggests that price spikes driven by geopolitical tension can fade once uncertainty begins to ease,” said Rick de los Reyes, a sector portfolio manager at T. Rowe Price. “But if production or exports face sustained disruption, that would amount to a genuine supply shock, with implications for inflation, interest rate expectations, and global growth.”

Hanging in the balance is the outlook for inflation, economic growth, interest rates, and the near‑term leaders and laggards in the stock market and other asset classes.

The only certainty now is that no one knows where this is going or how it will unfold. Several reasonable scenarios are plausible on paper. but when the fighting ends, the outcomes will almost certainly overturn many of today’s forecasts.

Is Recession Risk Rising? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

Author: James Picerno