Gulf’s Gray‑Zone Conflict Is Becoming a Market Stress Test

The military strikes of the past week have had little effect on markets to date, but it’s an open question how a low‑grade war will affect investor sentiment if the fighting drags on for weeks or months…Note, too, that a globally diversified portfolio has also rallied during this …

The Middle East conflict is a fire that seems to die down, only to flare up from embers that continue to burn. Those embers burned brighter over the weekend as the ongoing cycle of attacks between the US and Iran continued. The military strikes of the past week have had little effect on markets to date, but it’s an open question how a low‑grade war will affect investor sentiment if the fighting drags on for weeks or months.

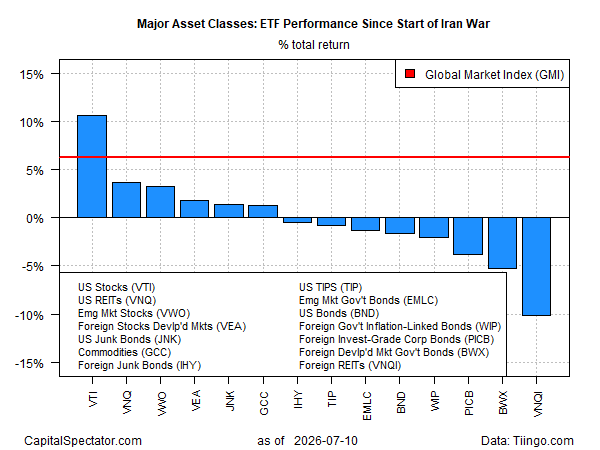

Reviewing the major asset classes since the first US strikes on Iran on Feb. 28 reminds us that the risk appetite was dented but not broken, based on a set of ETFs through Friday’s close. US equities have led the winners by a wide margin: the Vanguard Total Stock Market ETF (VTI) is up nearly 11% since the start of hostilities.

Note, too, that a globally diversified portfolio has also rallied during this period, advancing more than 6%, based on the Global Market Index (GMI), an unmanaged benchmark (maintained by The Capital Spectator) that holds all the major asset classes (except cash) in market‑value weights via ETFs.

Yet a fundamental question is coming into focus as the conflict drags on and the US confronts the possibility that military force, at least in its current form, may not achieve the administration’s aim of reopening the Strait of Hormuz and restoring pre‑war flow of energy exports.

Senior Iranian officials escalated their threats in recent hours as the latest U.S.–Iran exchange of strikes continued into Monday. Neither side appears to be backing away from a cycle of attacks that is unraveling the cease-fire signed last month.

The main question for markets is bound up with the outlook for inflation. Although oil prices have dropped sharply over the past month — briefly returning to pre‑war levels in early July — crude has rebounded in recent days, albeit moderately relative to the spike in March and April. Even if energy prices remain relatively stable in the near term, it’s unclear whether the recent surge of energy‑driven inflation is bleeding into the wider economy, which would likely require a response from the Federal Reserve. In that scenario, a series of rate hikes may be near, creating stronger headwinds for financial markets.

The prevailing narrative to date is that the Iran conflict lifted headline inflation via energy prices, but that this shift was temporary. This account is under renewed threat as it becomes clear that the US has few options for restraining Iran from attacking shipping in the Gulf. Short of a full‑scale invasion — an unlikely scenario — it’s possible, if not likely, that gray‑zone conditions in the Gulf, somewhere between war and peace, will persist. In turn, these conditions could support an ongoing inflationary pulse that triggers a reaction from the Fed.

The week ahead will be an important test of how markets price in the risk that hotter inflation may linger longer than recently expected. The US 2‑year Treasury yield is on the front line of digesting investor sentiment around inflation risk. An upside breakout above the recent peak of roughly 4.25% would be a worrisome sign for markets generally.

The United States has backed itself into a corner with Iran, trapped in a retaliatory cycle that leaves little leverage to defuse the crisis or accelerate a quick reopening of the Strait of Hormuz. If the waterway stays constrained for longer than expected, the resulting pressure on energy markets could keep inflation elevated well past policymakers’ comfort zone — and it’s increasingly unclear how markets will react to this emerging risk.

Author: James Picerno