Powell’s Pause: A Gamble Wrapped in Uncertainty

“The economic effects could be bigger, they could be smaller, they could be much smaller, they could be much bigger… But with so many moving parts to the conflict, and an endless array of rapidly evolving economic and financial implications, the distribution of outcomes could hardly be much wid…

The Federal Reserve has a deep pool of resources for analyzing the economy to support its mission to adjust monetary policy to match current and expected macro conditions. But sometimes a central bank’s vaunted research machine offers insights no sharper than whatever you’d get from chatting with a guy waiting at the bus stop. The present moment is one of those times, thanks to the uncertainty surrounding the ongoing war in Iraq.

Federal Reserve Chairman Powell admitted as much yesterday after the Fed announced that it left its key interest rate unchanged at a 4.50%-to-4.75% 3.50%-to-3.75% range.

“The thing I really want to emphasize is, nobody knows,” Powell said, citing the Iran war as the main source of indecision and uncertainty. “The economic effects could be bigger, they could be smaller, they could be much smaller, they could be much bigger. We just don’t know.”

No one does. One man in the White House holds the key for the war’s path, at least in terms of the US role. But with so many moving parts to the conflict, and an endless array of rapidly evolving economic and financial implications, the distribution of outcomes could hardly be much wider, or more shrouded in a fog of unknowing.

The main concerns from a macro perspective: the war could raise inflation, slow growth, or some degree of both – the dreaded stagflation scenario. The arrival of those twin challenges would be uniquely difficult for a central bank because the monetary toolbox tends to only work effectively on one problem or the other. That raises the difficult calculus that any decision could push one problem in the right direction while worsening the other. Tightening policy cools inflation but deepens unemployment, while easing policy supports hiring but fuels inflation.

The business of central banking goes on, of course, even if the best course of action in the current climate is to do nothing and wait to see what happens. .

One point of clarity for the market at the moment is that interest rate cuts are now considered unlikely any time soon. Before the war, the Fed funds futures market had been pricing in moderately high odds for a cut in June, but standing pat is now considered likely for the next seven policy meetings through Jan. 2027. Rate hikes aren’t expected, at least not yet, but in a sign of the times the crowd is now pricing in non-zero odds for the months ahead.

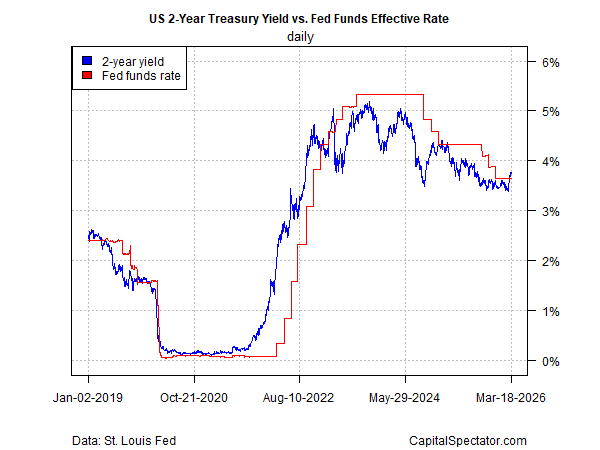

The Treasury market is also flirting with the possibility of rate hikes. For the first time in more than a year, the policy-sensitive 2-year Treasury yield (3.76%) is trading above the median effective Fed funds rate (3.64%), based on data through Wed., Mar. 18.

While the bond market is considering the chance that the Fed may have to raise rates at some point to combat a rise in inflation due to the war, the central bank’s collective outlook for the target rate is still expected to remain roughly unchanged or lower through the end of 2026, based on yesterday’s update of economic projections.

Commenting on the latest rate outlook by the Fed, Powell said: “If you notice, the median didn’t change, but there was actually some movement toward — a meaningful amount of movement — toward fewer cuts by people,” he noted in his press conference yesterday. “So, four or five people went from two to one, let’s say, two cuts to one cut.”

It’s all a guessing game in the extreme at the moment, which Powell effectively acknowledged:

“In the near term, higher energy prices will push up overall inflation, but it is too soon to know the scope and duration of the potential effects on the economy,” Powell said. “The thing I really want to emphasize is that nobody knows: the economic effects could be bigger, they could be smaller; they could be much smaller or much bigger; we just don’t know.”

That’s everyone’s mantra for the foreseeable future. No one knows, no one knows.

Sometimes the wisest move for a central bank is to stand still long enough to see whether the economy is actually moving or if inflation is rising. The danger, of course, is that waiting too long risks letting the inflation cat out of the bag. The Fed, presumably, learned that lesson during the inflation spike in 2022-2023.

It’s unclear if a repeat performance is brewing, or whether the central bank will have enough hard data to make an informed decision to minimize the risk. Like everyone else, the monetary gnomes will have to watch and wait, just like the rest of us.

Is Recession Risk Rising? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

Author: James Picerno