Rate Cuts on Ice as Inflation Expectations Surge at the Short End

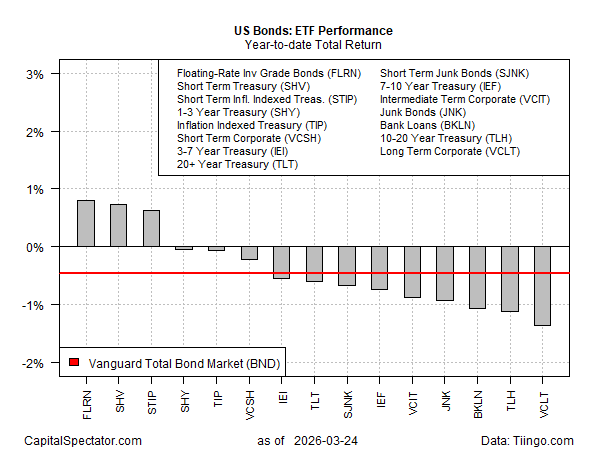

The hope is that the conflict will soon end, allowing Middle East oil and gas exports to resume, and thereby tame inflation worries… The upside outliers are limited to floating-rate investment-grade bonds (FLRN) and short-term Treasuries of the nominal and inflation-linked variety……

Inflation worries have convinced markets that the odds are low for a cut in interest rates this year by the Federal Reserve. Rate hikes are still considered unlikely, but the possibility is back on the table, if only on the margins. The change in sentiment, courtesy of the war in Iran, which has sent energy prices soaring, is weighing on the bond market. The hope is that the conflict will soon end, allowing Middle East oil and gas exports to resume, and thereby tame inflation worries.

At the moment, much of the fixed-income market is underwater this year, based on a set of ETFs through Tuesday’s close (Mar. 24). The upside outliers are limited to floating-rate investment-grade bonds (FLRN) and short-term Treasuries of the nominal and inflation-linked variety. The rest of the field has lost ground so far in 2026. The deepest year-to-date loss: long-term corporates (VCLT) via a 1.4% decline, substantially deeper than the 0.5% drop for the US investment-grade benchmark (BND).

Relief in the form of rate cuts is now considered unlikely for the near term. The Fed funds futures market is pricing in essentially zero odds for easing through the October policy meeting, shifting to a slight chance for a cut in December. A hike is also given low odds, but futures aren’t fully discounting the possibility.

For some analysts, the writing’s on the wall. “The market is saying that the Fed is done for the next year or two. We went from talking about how much the Fed is going to cut to how long the Fed is on hold for. The narrative has completely shifted in terms of what the Fed will do this year,” predicts Brij Khurana, a portfolio manager at Wellington Management.

A possible joker in the deck is the policy-sensitive 2-year Treasury yield, which has spiked higher in recent days. Trading just below 4.0% yesterday (Mar. 24), this proxy for rate expectations is now meaningfully above the median effective Fed funds rate (3.64%) for the first time in three years. That’s a sign that this corner of the bond market is anticipating tighter policy at some point.

A drop in energy costs could quickly change the calculus back to a neutral or disinflationary outlook, but a sentiment shift will require robust signs that inflation risk is tamer than the war-related risk implies. That will take time, given that formal inflation data arrives with a lag and it’s uncertain how, when or if the war will affect prices generally.

Reviewing breakeven rates in the Treasury market – a proxy for inflation expectations – paints a mixed picture. These estimates have surged on the short end of the curve. For example, the 1-year breakeven (nominal yield less its inflation-indexed counterpart) recently rose above 5%–a sign that investors are demanding a sharply higher inflation premium for the near term.

Longer-term inflation estimates are still modest and remain in a range that’s prevailed in recent history, which suggests that any inflation risk will be temporary. The 5-year breakeven, for example, has increased lately, but only modestly and is currently at 2.55%. That’s up from the recent low of 2.22%, but slightly below the roughly 2.60% high point for the last several years.

But confidence about the near-term future is still fluid. Until the war ends, and markets have time to assess how the macro outlook has changed, expectations for bonds, inflation, and interest rates will remain dependent on the duration of the conflict and the outlook for energy prices.

Author: James Picerno