Tehran Defies US as Conflict Escalates and Markets Reel

Although Iran will surely be transformed when the fighting stops, getting from here to there looks increasingly risky as the regime lashes out in a strategy to inflict maximum damage on the global economy by widening the conflict throughout the Middle East and thereby raising energy prices…Th…

Iran named Mojtaba Khamenei to succeed his slain father Ali Khamenei as the country’s supreme leader. The choice sends a signal that the country’s hardliners are still in control of the country and will remain defiant against President Trump’s demand for “unconditional surrender.” With neither side blinking, a quick end to the war, now in its tenth day, still appears elusive.

The main macro effect: oil prices on Sunday soared to nearly $120 a barrel for the US benchmark (West Texas Intermediate) before pulling back to just above $100 in early trading on Monday (Mar. 9). The spike marks the first return to triple-digit pricing in four years.

Assessing the risk outlook for the global economy boils down to a basic calculus: How long can Iran hold out?

The reasonable view: Not long. The combined military might of the US and Israel is vastly superior to Iran’s. But The Islamic Republic is fighting for its survival and is probably reasoning that it has little to gain from acceding to Washington’s demands. Although Iran will surely be transformed when the fighting stops, getting from here to there looks increasingly risky as the regime lashes out in a strategy to inflict maximum damage on the global economy by widening the conflict throughout the Middle East and thereby raising energy prices.

The US will almost certainly “win” in the end, but debate rages about the cost of victory and how the current conflict will reshape the Middle East and the politics of energy supplies.

Escalating the war won’t improve Iran’s odds of winning per se, but it will increase the pressure for a negotiated settlement in some form if public pressure ramps up in the West to end the fighting as a mechanism to lower energy prices.

Among the latest signs of Tehran’s strategy to widen the war, Saudi Arabia reported that its air defenses intercepted a new wave of airstrikes targeting Aramco’s giant Shaybah field. Expect more of these attacks to come.

The US is less vulnerable to an oil shock these days due to an increase in domestic production in recent years, a shift that’s has transformed America into the world’s largest oil producer and a petroleum exporter. In addition, the US economy, like most countries in the West, has become more energy efficient in recent decades and so the amount of oil needed to generate growth has fallen.

Despite this progress, the key macro challenge at the moment is that oil is still priced globally. Yale University Professor William Nordhaus presented a useful metaphor in a 2009 discussion that still applies today:

We can envision the oil market as a giant bathtub. The bathtub contains the world inventory of oil that has been extracted and is available for purchase. There are spigots from Saudi Arabia, Russia, the United States, and other producers that introduce oil into the inventory; and there are drains from which the United States, Japan, Denmark, and other consumers draw oil from the inventory. Nevertheless, the price and quantity dynamics are determined by the sum of these demands and supplies and the level of total inventory, and are independent of whether the faucets and drains are labeled “U.S.,” “Russia,” or “Denmark.”

The main economic risk from the war is stagflation. The longer the conflict lasts, the greater the threat of higher inflation and slower growth – a mix that is especially difficult to address through monetary policy. Raising interest rates can limit if not reduce inflation, but doing so at a time of rising energy costs will likely slow economic growth at a vulnerable time. The opposite is equally unappealing: cutting interest rates to stimulate growth, which could lift inflation even further for longer.

The solution, of course, is to end the war. The main uncertainty is when the economy crosses the Rubicon and an energy shock becomes unavoidable. The good news is that we’re probably not yet at the point of no return.

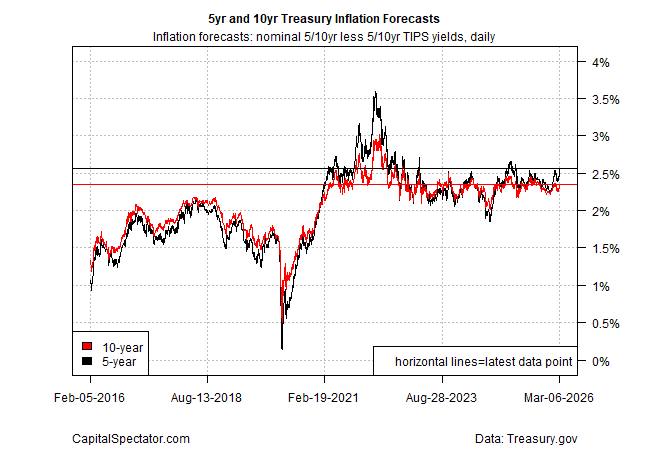

Market expectations for inflation have increased in recent days, but the current implied estimates via the Treasury market are still trading in the mid-2% range that’s prevailed over the last several years.

Meanwhile, the Dallas Fed’s Weekly Economic Index continues to reflect an upswing in economic activity through the end of February. The current 2.48% reading is slightly above the year-over-year GDP pace through the fourth quarter.

The threat that’s lurking is that the longer the fighting continues, the greater the possibility that the economic damage will deepen and linger.

The betting site Polymarket this morning is pricing in US recession risk for 2026 at 32%. That’s up about ten percentage points since the war started, but it still reflects optimism that growth will endure. So far, so good, the economic outlook will become increasingly precarious with each new day of war.

Is Recession Risk Rising? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

Author: James Picerno