The War May End Soon, But the Fed’s Battle Is Only Beginning

Unsurprisingly, sentiment has adjusted in recent days so that the 2-year yield is sticking close to the effective Fed funds rate – an implied forecast that the Fed will keep rates steady for the near term…Fed funds futures reflect a similar outlook and are pricing in expectations th…

Before the attack started on Feb. 28, lingering concerns about inflation had kept the Fed wary of extending last year’s interest rate cuts. Although several measures of pricing pressure had stabilized at lower levels relative to recent history, Fed officials expressed caution about declaring victory in fully taming the price spike that peaked at 9.0% year over year for the Consumer Price Index in June 2022.

The inflation trend has since fallen dramatically, and remained relatively stable in the mid-2% range, which is modestly above the Fed’s 2% target. But the cautious optimism that had accompanied the disinflation could be ancient history due to the war.

The concern is that the sharp rise in energy costs will reignite inflation and force the central bank to react by keeping monetary policy tighter for longer. It’s uncertain how long the surge in oil, gasoline and natural gas prices will last, and so it’s debatable how, if or when the Fed should respond. This gray area for policy will take time to clear. The longer the war lasts, the deeper the ambiguity about what comes next for policy decisions.

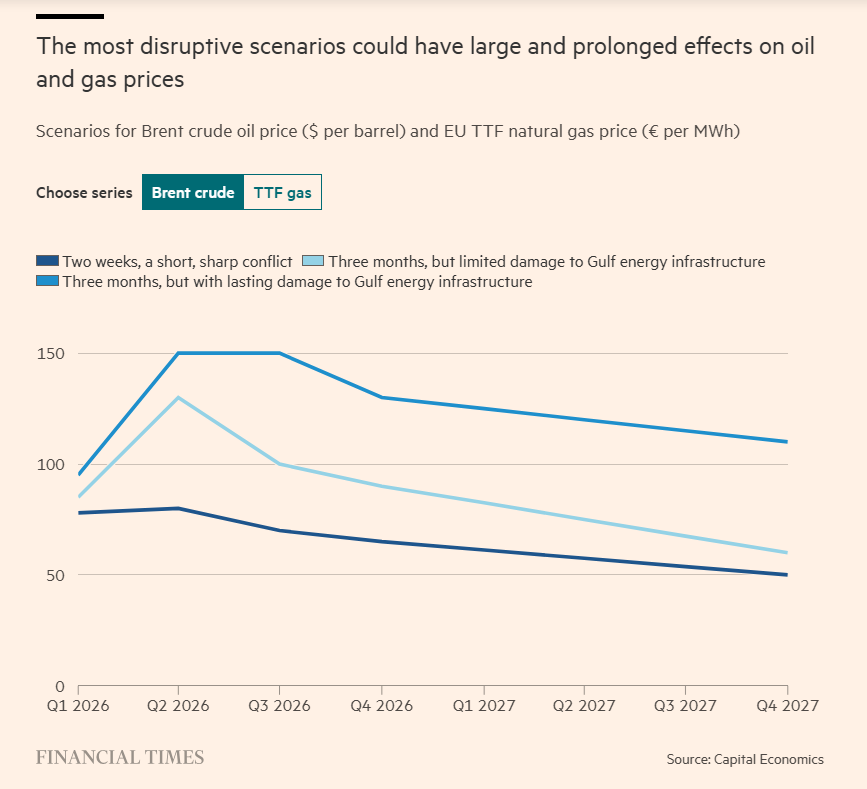

The critical questions: When will the war end, and what will follow in terms of economic consequences? It’s all speculation at this point, but analysts are considering an array of possibilities. Much of the analysis centers on how soon oil exports will rebound through the Strait of Hormuz, which remains essentially closed due to the war, and accounts for roughly one-fifth of the world’s seaborne exports. The basic calculus: the longer exports are blocked, the bigger the hit on supply, which in turn will bring longer-lasting upside pressure to energy prices, estimates Capital Economics via the FT.

The challenge for the Fed is deciding which scenario is likely, and setting monetary policy appropriately. But with no clear end to war in sight as of this writing, the near-term outlook is as cloudy as ever for energy costs and the implications for inflation and economic growth.

Markets are struggling to price in the possible scenarios and insteada are favoring a wait-and-see approach. Consider the policy-sensitive US 2-year Treasury yield, which is widely followed as a proxy for the Fed’s expected policy stance. Unsurprisingly, sentiment has adjusted in recent days so that the 2-year yield is sticking close to the effective Fed funds rate – an implied forecast that the Fed will keep rates steady for the near term.

Fed funds futures reflect a similar outlook and are pricing in expectations that the central bank will leave rates unchanged for the next three policy meetings. The odds start to favor a rate cut in July or September, but those estimates should be viewed cautiously given the depth and breadth of uncertainty at this point about how the war will impact growth and inflation in the months ahead.

“The Fed always has a problem on how to respond to a supply shock,” said Alan Detmeister, a former Fed economist who’s currently at UBS. “On the one hand, the inflationary aspects suggest you should be raising interest rates. On the other, the reduced output and increased unemployment suggest you should be lowering interest rates. It’s not clear, and it just causes the Fed to wait and see which part of their dual mandate they think needs the biggest help.”

In the end, a ceasefire at some point may calm the region, but the potential for economic aftershocks won’t provide clarity for the Fed’s calculus anytime soon.

Is Recession Risk Rising? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

Author: James Picerno