Treasury Premium Climbs Again, Fueled by Sticky Inflation

The threat of higher inflation stemming from the Iran conflict remains a risk factor, though the repricing of the market premium has been modest so far…The gradual shift may begin to accelerate in the months ahead as inflation risk moves to center stage in the bond market… The recent upsi…

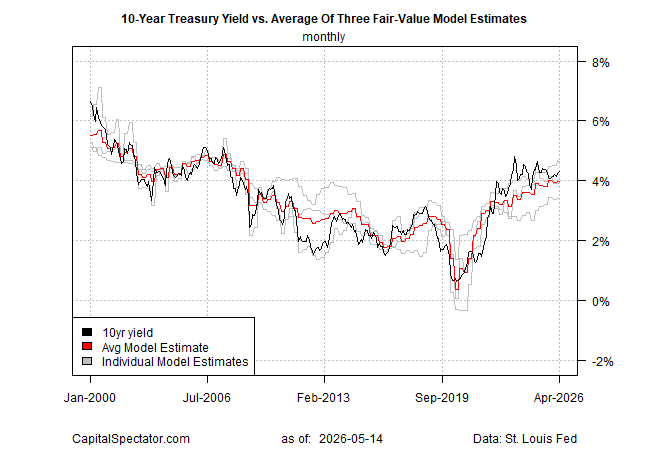

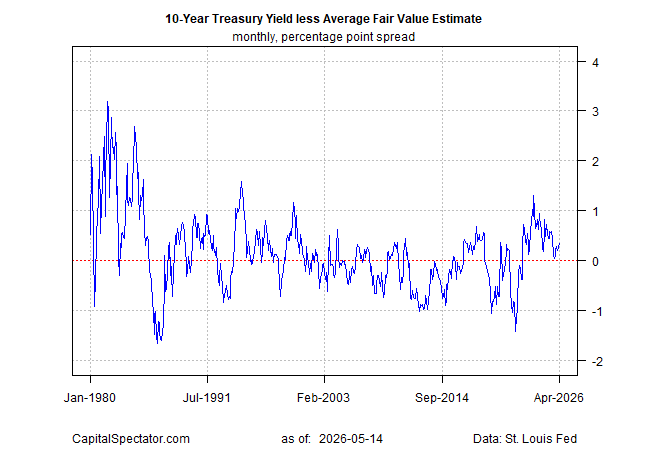

The market premium for the US 10-year Treasury yield over a fair‑value estimate remained modest in April but has been edging higher after falling to a near‑equilibrium level late last year. The threat of higher inflation stemming from the Iran conflict remains a risk factor, though the repricing of the market premium has been modest so far.

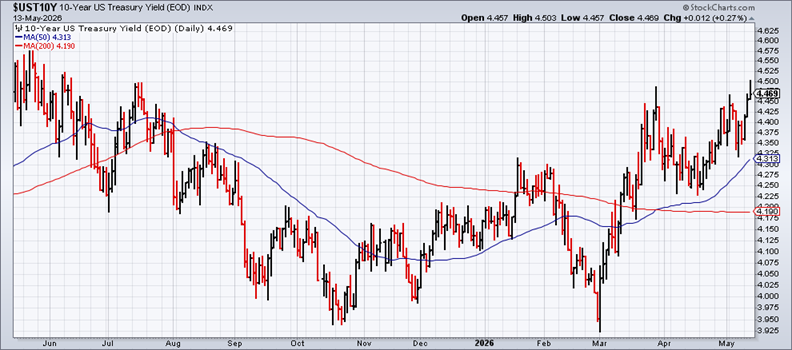

The gradual shift may begin to accelerate in the months ahead as inflation risk moves to center stage in the bond market. The 10‑year yield rose to 4.47% yesterday (May 13), the highest close since last August. The recent upside bias suggests that the pickup in inflation triggered by the Middle East turmoil is starting to alter sentiment for fixed‑income securities.

The Labor Department reported this week that consumer and wholesale inflation continued to post sharp increases in April.

“Inflation is sticky and accelerating. The core reading confirms a deeper structural trend, especially in services,” said David Russell, global head of market strategy at TradeStation. “The Hormuz crisis is aggravating the problem, but this goes way beyond oil.”

The market premium relative to The Capital Spectator’s fair‑value estimate of the 10‑year yield ticked up to 35 basis points last month. That remains modest by historical standards, but if inflation stays elevated—or shows signs of rising further—the premium will likely increase in the months ahead.

“

What we’ve seen is investors pricing in higher long‑term inflation into what they want to receive from lending to the government,” said Luke Tilley, chief economist at Wilmington Trust.

By late 2025, the surge in the 10‑year premium associated with the 2021–2022 inflation spike had faded to nearly zero. But the calculus is changing as the conflict with Iran continues and threatens to become a protracted affair that keeps Gulf energy exports blocked and inflation elevated.

A quick resolution that allows exports to resume would likely keep the yield premium modest. But with diplomatic efforts at a standstill and US threats to resume military operations if Iran doesn’t compromise, the timeline for an end to the conflict remains unclear. As a result, the yield premium—and interest rates more broadly—appear poised to rise in the near term.

Is Recession Risk Rising? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

Author: James Picerno