US 10‑Year Treasury Yield Near ‘Fair Value’ at Outset of Iran War

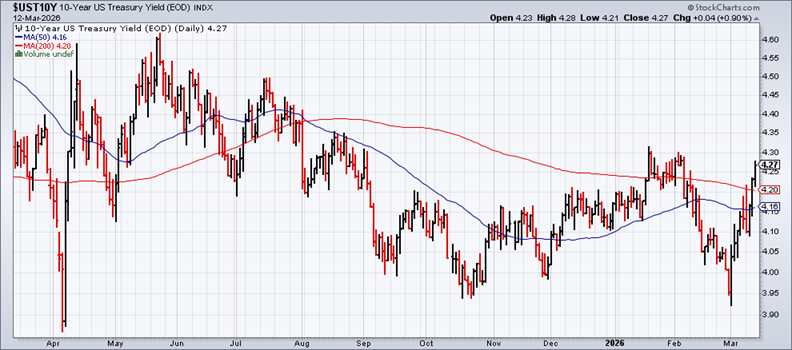

The 10-year Treasury yield was close to its “fair value” estimate in February, based on the average of three models…The 10-year yield in March has jumped more than 30 basis points since last month’s close, rising to 4…Using the 10-year yield as a proxy, the market appears to be …

The 10-year Treasury yield was close to its “fair value” estimate in February, based on the average of three models. Before the start of the war in Iran on Feb. 28, the fading market premium in recent months was expected to continue, and perhaps slide to a discount in the near future. The outlook has been upended due to the ongoing military conflict, which is sending shock waves through the world economy.

The 10-year yield in March has jumped more than 30 basis points since last month’s close, rising to 4.27% on Thursday (Mar. 12). A key driver in the yield’s rebound: increasing concern that the surge in energy costs related to the war will lift inflation for some period of time.

The counterview is that the war’s end will ease inflation risk, but it’s unclear how long lingering effects from the disruption to energy supplies will reverberate. The general consensus: the longer the war lasts, the greater the risk that inflation will rise well into the future.

Using the 10-year yield as a proxy, the market appears to be repricing inflation risk, albeit moderately so far. The 10-year rate’s rise so far this month leaves it at a middling level relative to recent history. A decisive and sustained move above 4.30% (the previous peak), however, would signal increasing concern that energy-related risk for inflation won’t quickly fade when the war ends.

Heading into the war, the market premium for the 10-year yield was roughly 20 basis points in February, according to CapitalSpectator.com’s ensemble model. That’s in line with recent months, which reflects a sharp slide from the high premium that prevailed over the past several years.

It’s unclear if investor sentiment will demand a higher premium – again – in the months ahead. The key variable is how the war in Iran unfolds in the days (weeks?) ahead, and how the conflict influences energy costs.

For now, the bond market is pricing in higher reflation risk, albeit moderately so far. The question is whether energy costs normalize after the war. Some analysts are skeptical of a quick return to pre-war prices.

“Too much geopolitical risk has been exposed,” says Blerina Uruçi, chief U.S. economist at T. Rowe Price. She forecasts that it’s unlikely that oil will soon trade below $80 per barrel, much less return to the pre-war $60 range.

“I don’t think that’s going to normalize anytime soon.”

The US crude oil benchmark, West Texas Intermediate, has pulled back from its intraday peak of roughly $120, but Thursday’s $96 reminds us that a return to “normal” still doesn’t look imminent.

Author: James Picerno