US Q1 GDP May Improve As War Threatens the Outlook

US economic growth in the first quarter is still expected to rebound from the sluggish rise in Q4, but macro storm clouds are gathering for Q2 as the war in Iran continues… On that basis, growth will recover some of the lost momentum in Q4, when the economy expanded by a weak 0…4 this month, an …

US economic growth in the first quarter is still expected to rebound from the sluggish rise in Q4, but macro storm clouds are gathering for Q2 as the war in Iran continues.

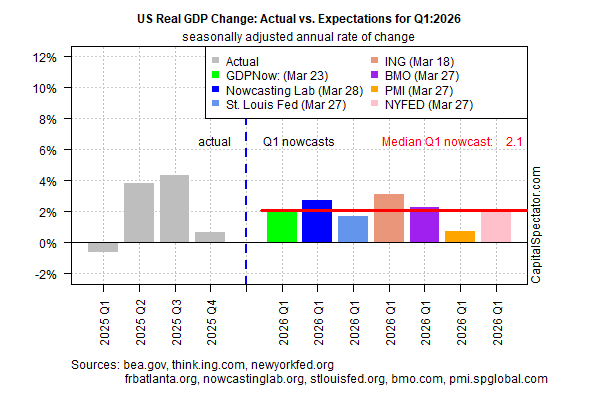

The current nowcast for Q1 indicates an annualized 2.1% increase, based on the median estimate from a set of nowcasts compiled by The Capital Spectator. On that basis, growth will recover some of the lost momentum in Q4, when the economy expanded by a weak 0.7%.

Today’s Q1 estimate is down slightly from the previous update (Mar. 16). Further downgrades are possible, if not likely, between today and April 30, when the Bureau of Economic Analysis publishes its initial GDP estimate for Q1. Most of the economic data for the first three months of the year are expected to reflect pre-war activity. Although it’s unclear how the war has affected output in March, the fallout will probably be limited.

PMI survey data, however, suggest a non-trivial headwind in March. The US Composite PMI Output Index, a GDP proxy, fell to 51.4 this month, an 11-month low that reflects a weak growth bias. “The flash PMI survey data for March signal an unwelcome combination of slower growth and rising inflation following the outbreak of war in the Middle East,” says Chris Williamson, chief business economist at S&P Global Market Intelligence.

Joseph Brusuelas, chief economist at RSM, a consultancy, today writes: “Financial markets in the United States are pricing in a longer duration of the war in the Middle East. Our RSM US Financial Conditions Index, which has been decelerating since early February, has turned negative, implying a modest drag on growth.”

Deciding if a modest drag on growth deteriorates into something worse for Q2 will be determined by how the war evolves in the days and weeks ahead. Perhaps the only calculus that’s reliable at this point: the longer the conflict persists, the greater the economic damage.

The odds still suggest the US will avoid a recession starting at some point this year, according to Polymarket, a betting site. But this morning’s 37% chance of contraction by the end of 2026 has increased from 23% at the start of the war.

Some analysts say that markets are overreacting to the risks posed by the war. But with no sign of an end to the fighting on the immediate horizon, the potential threat to the global economy, with spillover effects for the US, will become harder to dismiss in the days ahead.

“Every recession since World War II, save the pandemic recession, has been preceded by a spike in oil prices,” Mark Zandi, chief economist at Moody’s Analytics, wrote last week. “Higher oil prices do not do the same economic damage as in years past, because the US produces as much as it consumes. But consumers still get hit hard and fast while producers invest and hire more only slowly, if at all, waiting to make sure the higher prices are here to stay.”

Is Recession Risk Rising? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

Author: James Picerno